The calendar doesn’t lie: you have 30 days until June 15, 2026 — the Q2 estimated tax deadline for freelancers and self-employed professionals. Miss it, and the IRS won’t send a gentle reminder. They’ll send a penalty. But if you start today, you have exactly enough time to calculate what you owe, organize your deductions, and pay with confidence. Here is your complete week-by-week action plan.

Why the June 15 Deadline Matters — And What Happens If You Miss It

The U.S. tax system operates on a pay-as-you-go basis. Employees have taxes automatically withheld from each paycheck. Freelancers, independent contractors, and self-employed individuals must make quarterly estimated tax payments four times per year. Q2 covers income earned from April 1 through May 31, 2026, with payment due by June 15.

If you underpay — or skip the payment entirely — the IRS charges an underpayment penalty of 0.5% per month on the unpaid balance. That rate compounds over time and can climb even higher if the balance remains unpaid after the annual filing deadline. The penalty feels small until you realize it applies to every quarter you miss, stacking up across the year into a bill that can easily reach hundreds of dollars.

The good news: avoiding penalties does not require perfection. It requires enough. The IRS provides two safe harbor rules:

- Safe Harbor 1: Pay at least 100% of what you owed in federal taxes for 2025. If your 2025 adjusted gross income exceeded $150,000, pay 110% of last year’s tax.

- Safe Harbor 2: Pay at least 90% of your estimated 2026 tax liability across all four quarterly payments.

Meet either threshold and the underpayment penalty disappears — even if you end up owing more when you file in April 2027. With 30 days on the clock, here is exactly what to do each week.

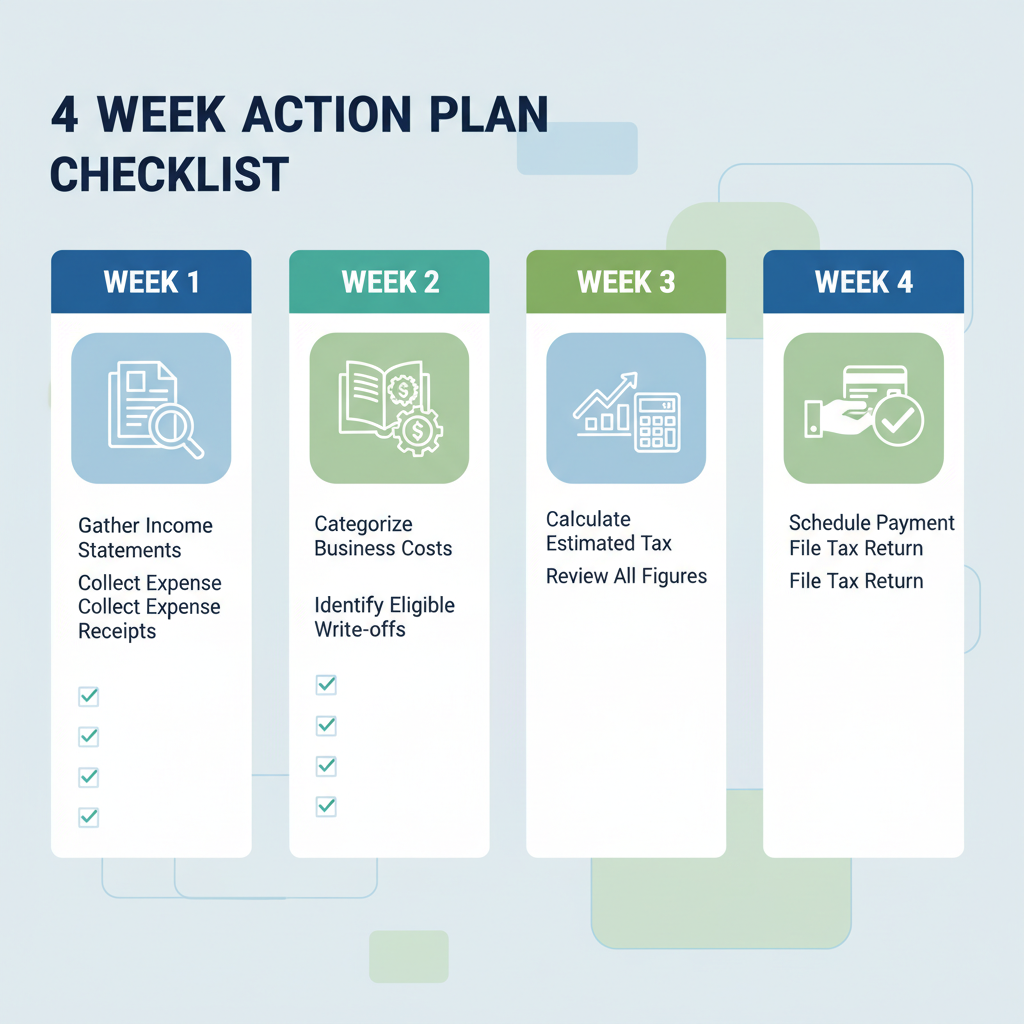

Week 1 (May 16–22): Gather Income and Calculate Your Base

The first week is all about numbers. Pull together every source of freelance income you received between January 1 and May 31, 2026. This includes:

- Payments from clients, platforms, and marketplaces

- 1099-NEC or 1099-K forms already received (note: many arrive later, so don’t wait for paper forms)

- Bank deposits, PayPal transfers, Venmo business payments, Stripe payouts, and any cash income

- Income from short-term rentals, royalties, or gig economy platforms

Once you have your gross income figure, estimate your self-employment tax. The SE tax rate is 15.3% on net self-employment earnings up to $176,100 (2026 threshold), covering both the employee and employer portions of Social Security and Medicare. You can deduct half of that SE tax from your gross income before calculating ordinary income tax.

Apply your federal marginal rate (10%, 12%, 22%, 24%, etc.) to the taxable income figure. Add SE tax + income tax together, subtract any payments already made for Q1 (April 15), and divide by four. That is a reasonable estimate of what one quarter’s payment should be.

Tools that help: IRS Form 1040-ES includes a worksheet for this exact calculation. The IRS also provides an online Tax Withholding Estimator you can use for free.

Week 2 (May 23–29): Maximize Your Deductions

Before you finalize your estimated payment, spend Week 2 identifying every legitimate deduction. Business expenses directly reduce your net self-employment income — lowering both SE tax and income tax simultaneously. Common deductions for freelancers include:

- Home office deduction: If you use a dedicated space exclusively for work, you can deduct a proportional share of rent, utilities, and internet.

- Software and subscriptions: Project management tools, design apps, communication platforms, accounting software — all deductible if used for business.

- Equipment and devices: Laptops, cameras, microphones, monitors purchased in 2026 may qualify for Section 179 immediate expensing.

- Health insurance premiums: Self-employed individuals can often deduct 100% of health insurance premiums paid for themselves and their families.

- Business travel and mileage: The 2026 standard mileage rate applies to any business-related driving. Keep a log.

- Professional development: Courses, certifications, books, and industry conferences directly related to your field.

- Retirement contributions: Contributions to a SEP-IRA, Solo 401(k), or SIMPLE IRA reduce your taxable income and can still be made for 2025 until the filing deadline.

Every dollar in legitimate deductions is a dollar not subject to the 15.3% SE tax. At higher income levels, reducing your taxable income by $5,000 in deductions can cut your estimated payment by $750 or more. Do not leave this money on the table.

Week 3 (June 1–7): Verify, Adjust, and Prepare Your Payment

By Week 3, you should have a solid estimate of what you owe. Now it is time to verify your math and prepare to pay. Check the following:

- Confirm safe harbor coverage. Pull your 2025 tax return and note the total tax shown on Line 24 of Form 1040. Divide by four. If your Q2 payment covers at least one-quarter of that amount (or one-quarter of 110% if your AGI exceeded $150,000), you are protected from the underpayment penalty regardless of what you ultimately owe in April.

- Account for any Q1 overpayment or underpayment. If you overpaid in Q1, you can credit that amount toward Q2. If you underpaid, factor in the shortfall.

- Create your IRS account if you haven’t. Go to IRS.gov — Your Online Account to view your payment history, confirm prior payments were received, and set up your Q2 payment in advance.

This week is also when you should set up the actual payment method. The IRS accepts several options:

- IRS Direct Pay — Free bank transfer from checking or savings. No fee. Available 24/7 at IRS Direct Pay.

- EFTPS (Electronic Federal Tax Payment System) — Free, but requires advance enrollment (allow up to 5 business days). Best for recurring quarterly payers.

- Debit or credit card — Accepted via IRS-authorized processors with a processing fee (typically 1.82–1.98% for credit cards, $2.14–$2.50 flat fee for debit).

- Check or money order — Mailed with Form 1040-ES voucher. Must be postmarked by June 15.

Week 4 (June 8–15): Pay, Confirm, and Document

The final week is execution week. Do not wait until June 15 to pay — banking delays, website traffic spikes, and technical issues all increase risk the closer you get to deadline. Pay by June 12 at the latest if using a bank transfer. If mailing a check, send it by June 10 to ensure it is postmarked in time.

After paying:

- Save your confirmation number. IRS Direct Pay and EFTPS both generate confirmation numbers. Screenshot it or write it down. You will need this if there is ever a dispute about whether your payment was received.

- Log the payment in your records. Note the date, amount, payment method, confirmation number, and the tax period it covers (Q2 2026).

- Update your income tracking. Record any income received in June that will apply to Q3 (July 15 deadline). Getting ahead of Q3 now makes that payment far less stressful.

The 30-Day Advantage: Why Acting Now Changes Everything

Most freelancers wait until the week before the deadline to start thinking about estimated taxes. By then, there is no time to find deductions, verify numbers, or correct mistakes. Starting today gives you a significant advantage: you can reduce your payment legally through deductions, protect yourself with safe harbor coverage, and pay without panic.

The freelancers who consistently avoid IRS penalties are not the ones who earn the most — they are the ones who track their income and expenses throughout the year. Every receipt, every invoice, every business expense logged in real time means less scrambling each quarter.

Thirty days is enough time to get this right. Start with Week 1 today, and by June 15 you will have checked the box with zero penalties and full confidence.

Track your freelance income and expenses automatically — and know exactly what you owe each quarter. Download BudgetX free and never miss a tax deadline again.